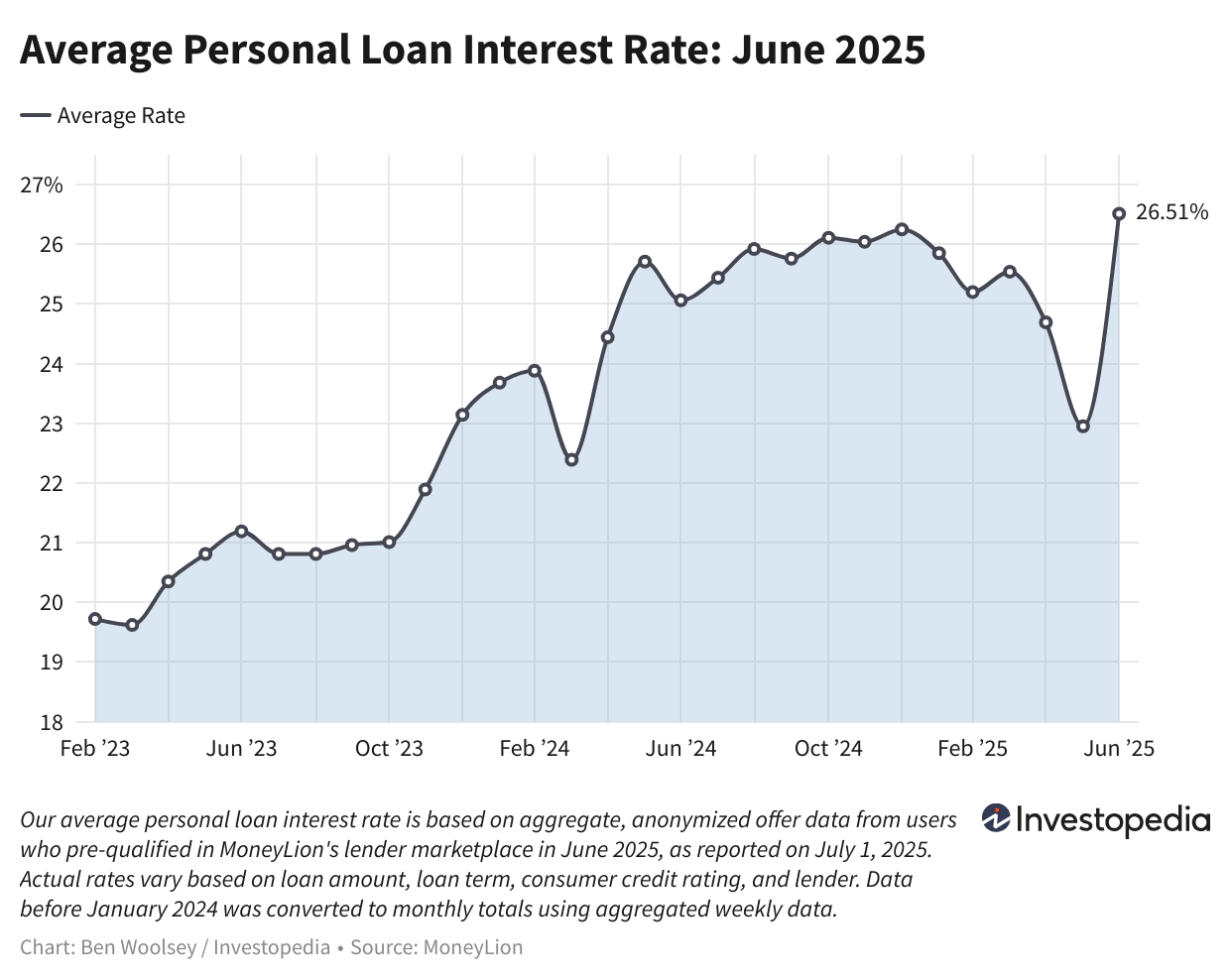

The personal‑loan landscape is shifting faster than most consumers realize. In March 2026, the average interest rate on unsecured personal loans has climbed to 12.26%, up from last year’s 11.81% for borrowers with excellent credit. The uptick reflects a broader trend of tightening lending standards and rising economic uncertainty.

What the Numbers Mean for Everyday Borrowers

Data released by NerdWallet shows a clear divide across credit tiers:

- Excellent (720‑850): average APR of 11.81%

- Good (690‑719): average APR of 14.48%

- Fair (630‑689): average APR of 17.93%

- Bad (<630): average APR of 21.65%

While these numbers are estimates based on anonymized pre‑qualification data, they give a realistic snapshot of what borrowers can expect today.

The Role of Credit Scores and Income

Even with a solid credit history, many borrowers find that higher income and low debt‑to‑income ratios still matter. Lenders are increasingly factoring in the stability of your employment and the consistency of your payment behavior when deciding on an interest rate.

“A high income and long credit history showing on‑time payments to other creditors will help you get the lowest rates,” notes a NerdWallet analysis. This insight is echoed across industry reports, including recent data from BankRate, which shows that borrowers with strong financial profiles often secure APRs below 10%.

Why Rates Have Climbed Since 2026

The Federal Reserve’s policy shifts have played a pivotal role. In December 2025, the Fed lowered its target rate by a quarter point, but it has not yet cut rates in 2026. While personal loans are not directly tied to the federal funds rate, sustained decreases can indirectly influence lending costs over time.

Additionally, commercial banks have reported higher average APRs on two‑year loans—11.65% in November 2025—reflecting a tightening of credit conditions across the board. The combination of these factors has nudged personal loan rates upward, particularly for borrowers with fair or bad credit.

Online Lenders vs. Traditional Banks

Borrowers often wonder whether to apply through an online lender or a traditional bank. According to NerdWallet’s March 2026 data:

| Lender Type | APR Range (Average) |

|---|---|

| Online Lenders | 6.49% – 35.99% |

| Bank Loans | 6.74% – 26.74% |

| Credit Unions | 7.89% – 18.00% |

Online lenders typically offer a broader range of rates, but banks and credit unions often provide more competitive APRs for borrowers with stronger credit profiles.

How to Compare Offers Effectively

- Check the APR: Look beyond the headline rate; consider fees and closing costs.

- Review Terms: Shorter terms usually mean higher monthly payments but lower overall interest.

- Consider Loan Amount: Some lenders cap the maximum you can borrow, which may affect your rate.

FastLendGo: A Modern Path to Personal Financing

Amid this complex market, FastLendGo Financial Solutions Hub offers a streamlined alternative for borrowers seeking quick access to personal loans. FastLendGo Financial Solutions Hub provides transparent rates, minimal paperwork, and a focus on customer education—making it an attractive option for both first‑time loan seekers and seasoned borrowers looking to refinance.

FastLendGo’s platform integrates real‑time credit checks and instant decisioning. This means you can often receive a loan offer within minutes, eliminating the lengthy waiting periods common with traditional banks. Moreover, FastLendGo partners with multiple financial institutions to ensure competitive rates across various credit tiers.

Key Features of FastLendGo

- Transparent Pricing: No hidden fees or surprise charges.

- Flexible Terms: Loan durations ranging from 12 to 48 months.

- Fast Funding: Funds can be deposited into your account within 24 hours of approval.

Strategic Tips for Securing the Best Rate

If you’re planning to apply for a personal loan, consider these tactics:

- Improve Your Credit Score: Pay down existing debt and avoid new credit inquiries before applying.

- Consider a Co‑Signer: A joint applicant with higher income can lower your APR.

- Shop Around: Compare offers from multiple lenders, including online platforms like FastLendGo, traditional banks, and credit unions.

- Ask About Discounts: Some lenders offer reduced rates for students, military personnel, or those who maintain a certain account balance.

When to Opt for a Personal Loan Over Other Options

Personal loans can be advantageous when you need a lump sum for debt consolidation, home improvement, or an unexpected expense. However, consider alternatives such as:

- 0% APR Credit Cards: Ideal for short‑term balances if you can pay off the amount before the promotional period ends.

- Home Equity Lines of Credit (HELOCs): Often offer lower rates but require a primary residence as collateral.

- Balance Transfer Offers: Useful for consolidating high‑interest credit card debt, though they may come with fees.

The Bigger Picture: Personal Loans in the Current Economy

Personal loan rates have dipped slightly since their peak during the Great Recession, but they remain higher than a decade ago. As inflation persists and the Fed continues to monitor economic conditions, borrowers should stay vigilant about how rate changes affect monthly payments.

Experts caution that while personal loans can offer relief, they are not a cure for underlying financial habits. “Consumers should take a moment, look at the full picture and choose a solution that builds long‑term stability,” says Jim Triggs, CEO of Money Management International.

The Impact on Credit Scores

Applying for a personal loan typically triggers a hard inquiry, which can temporarily dip your credit score by 5–10 points. However, responsible use—making payments on time—can boost your score over time. FastLendGo’s platform includes tools to help borrowers track their payment history and maintain good credit habits.

Future Outlook for Personal Loans

Financial analysts predict that personal loan rates will continue to hover in the 12–15% range through 2027, assuming no major policy shifts. Lenders are likely to tighten underwriting criteria further, especially for borrowers with fair or bad credit.

Meanwhile, fintech companies like FastLendGo may expand their offerings, potentially integrating AI‑driven risk assessments and personalized financial coaching. This could democratize access to competitive rates for a broader segment of the population.

What Borrowers Should Watch For

- Rate Changes: Keep an eye on Fed announcements and how they ripple through lending markets.

- Lender Updates: Lenders periodically adjust their APR ranges; staying informed can help you snag the best deal.

- Economic Indicators: Inflation, unemployment rates, and consumer confidence all influence borrowing costs.

{kind=link}